FAQs

-

Documents and Links Referenced in This Section

- Attorney General's website

- Buyer Partner Listing (requires KSU login to access)

- Catering Request form

- Checking the status of a requisition

- Clearing Browser Cache

- Compliance Food Approval website

- Concur User Profile Action Form

- Contract Management System

- Contract Submission Form

- Current Stationery Pricing

- Current University Contracts

- Department of Administrative Services (DOAS) Exempt Items List

- Department of Administrative Services Fleet Management Division

- DHS E-Verify website

- Environmental Health and Safety Department website

- E-Verify Affidavit

- E-Verify FAQs

- E-Verify FAQs website

- Food Documentation Form

- Georgia Procurement Manual (GPM)

- Georgia Technology Authority (GTA) website

- How to Access GeorgiaFIRST Marketplace

- How to Create a GeorgiaFIRST Marketplace Requisition

- How to Create an ePro Special Request Requisition

- Independent Contractor vs. Employee Checklist

- KSU Charter Services Policy website

- KSU Policy Portal

- KSU’s Visual Identity Program website

- More Business Solutions ordering portal

- PeopleSoft Access Form (requires access to KSU Connect)

- Printing Services vs. Promotional Services Overview Guide

- SSN/ITIN Procedures

- Statewide Purchase Order Policy

- Statewide Purchase Orders Policy

- Stationery Quick Start Guide

- Steps to Hire a Temporary Worker

- Team Georgia Marketplace

- Technology Purchases website

- Temporary Staffing Statewide Contracts

- Travel FAQs - Lecturers and Performers

- UITS - Other Technology Request Forms

-

How Do I Buy ...

-

Goods & Services

University Contracts that have already been bid and awarded by the Office of Procurement for services that are routinely needed for the University’s operation can also be utilized by any department. Departments may also utilize contracts that have been bid and awarded by DOAS (Statewide Contracts) for specific services. Orders placed using University Contracts and Statewide Contracts are not subject to dollar limits. The Office of Procurement can assist departments with determining whether University Contracts or Statewide Contracts are available resources for securing the service(s) needed. Please note that if a Contract is required by the Supplier in order to perform the service, then the Contracts Office must review and approve the proposed contract. If the desired service is being procured from a University Contract, a Board of Regents, or Statewide Contract, then additional review from the Contracts Office is not needed, unless customizations and/or modifications to the contracted service is required to successfully accomplish what is required for the University. A Contract Submission Form must be completed online prior to signing any contract.

NOTE: A Purchase Order is a contract, and a Terms and Conditions document is provided with each purchase order that is sent to a supplier. When suppliers accept a purchase order, they are in effect accepting the University’s offer to purchase services and goods under the terms and conditions outlined therein, unless a separate contract is negotiated and executed by both parties and incorporated as part of the purchase order contract.

It is important to involve the Office of Procurement early in the purchasing process to ensure that all requirements are addressed prior to the performance of services, as well as ensuring that the requesting department does not experience delay in delivery of the services needed.

Per the State Accounting Office (SAO) Statewide Purchase Order Policy, all purchases $2,500 or more require the use of a Purchase Order (PO). All purchases involving services totaling $2,500 or more requires a completed and notarized E-Verify Affidavit.

Generally, purchases up to $9,999.99 can be done by a college or department using the GeorgiaFIRST Marketplace or by submitting an ePro Special Request to obtain a purchase order for the item(s) needed.

Purchases for $10,000 up to $24,999.99 must be procured by securing competitive quotes from at least three (3) suppliers. Once you have the three quotes, submit an ePro Special Request so that the Office of Procurement can create a Purchase Order prior to ordering the good(s) from the selected supplier.

Purchases over $25,000 must be competitively bid if the purchases are non-exempt and do not already fall under an existing University (Agency) or Statewide Contract.

Goods or services may also be ordered utilizing University contracts that may have already been bid and awarded by the Office of Procurement for that particular category of items needed.

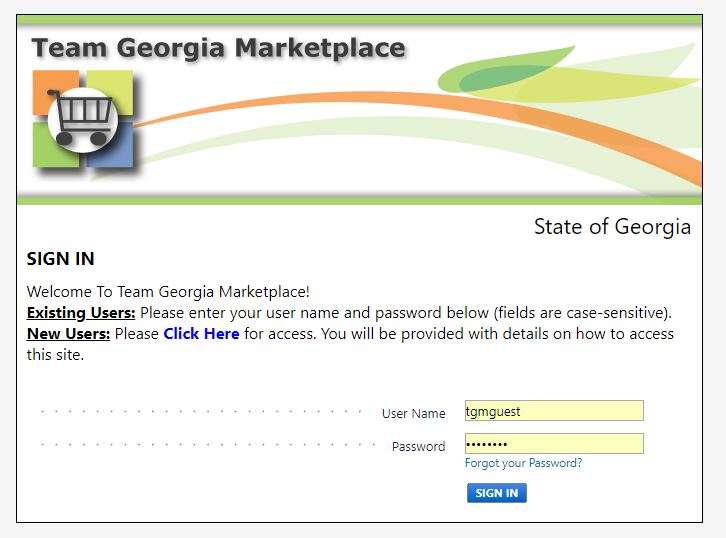

You may also use contracts that have been bid and awarded by Department of Administrative Services (DOAS) Statewide Contracts, many of which are listed on the GeorgiaFIRST Marketplace. A complete list of State contracts can be found on the Team Georgia Marketplace. Please note that the User Name and Password are both “tgmguest" (all lowercase and without quotes).

Orders placed using University and Statewide contracts are not subject to any of the dollar limits mentioned above. Please contact service.kennesaw.edu/ofs or call 470-578-6214 if you would like further guidance on using University or State contracts.

-

Ink Cartridges & Office Supplies

Office supplies can be purchased from Staples through the GeorgiaFIRST Marketplace located in PeopleSoft. Department ePro Requesters can access the catalog via the eProcurement menu option in PeopleSoft.

To purchase ink cartridges from Staples, or other items that are listed as "Restricted" on the GA First Marketplace, please reach out to our Staples representative listed below either through the email address or phone number provided:

Live chat on staplesadvantage.com

Email: support@StaplesAdvantage.com

Call: 877-826-7755

Monday-Friday 8am – 8pm ETThe Staples representative will supply a quote for the items that you may either order via P-Card (if allowable) or through a Special Request Requisition.

-

Miscellaneous Items

-

Food

A Food Documentation Form must be completed, signed and submitted with all food purchases by the business manager or another authorized individual in your department. The authorized approver in your department/college is required to sign the KSU Guidelines for Food Purchases on an annual basis.

Additional approval is requested for all employee group meals from service.kennesaw.edu/ofs prior to the date of the event to obtain authorization from the President.

All purchases paid with an agency fund or grant must have a written approval from the respective office prior to the food purchase.

-

FurnitureFurniture purchases can only be made from Statewide Convenience Contracts managed by the Department of Administrative Services (DOAS). For guidance in using the services of a manufacturer’s representative, please contact the Division of Facilities Services via email (facilities@kennesaw.edu) or by phone (470-578-6224).

-

Lab Supplies

Follow the procedures for purchasing “Goods.” There are with suppliers such as Fisher Scientific, VWR, and Carolina, which can be accessed through the GeorgiaFIRST Marketplace in the form of punch-out catalogs.

Please note that purchases involving toxic or radioactive materials must start with notification and approval from the KSU’s Environmental Health and Safety Department.

Certain laboratory supplies are exempt from procurement regulations. The Department of Administrative Services (DOAS) provides a list of exempt items. However, departments should contact the Office of Procurement to ensure that the desired purchase meets the intent of the exemption.

-

-

Printing & Promotional Services

-

Printing Services vs. Promotional Services OverviewThe Printing Services vs. Promotional Services Overview Guide provides an overview of the differences between promotional services and printing services. This guide also includes situations in which you may go off-contract to purchase printing or promotional items and what types of approvals are required for the type of purchase needed.

-

AdvertisingMost forms of advertising are exempt from DOAS purchasing requirements for competitive bidding, and departments may follow “How do I Buy Services” guidelines. In addition, printed materials that incorporate University logos, service marks, or other University-related design elements must comply with KSU’s Visual Identity Program.

To have the design/artwork pre-approved through the Office of Strategic Communications and Marketing, email requests to designapproval@kennesaw.edu prior to placing an order and/or making a purchase.

Advertising is a service; therefore, E-verify compliance is required. Additional E-Verify FAQs are located on Procurement’s E-Verify FAQs webpage. -

Business Cards/Letterhead/Stationery

Stationary may be purchased through our University contract with More Business Solutions. This is the only type of purchase that uses the University’s name or logo that does not require Design Approval.

There are two ways to order business cards and stationery for your department. The first, and easiest way, is to use a Purchasing Card (P-Card). The second way, if your department does not have a P-Card, is to use a Purchase Order.

The More Business Solutions ordering portal, along with the Stationery Quick Start Guide and current pricing documentation, can be found under the "Documents and Links Referenced in This Section" towards the top of this page.

-

Ordering Stationery Using a P-Card

To place an order using a P-Card, navigate to the More Business Solutions ordering portal. If you need to create an account, you can find the guide below. You will then create your order using the templates found on the portal, using the information for each person or department that you are ordering for. At the checkout screen, you will choose Credit Card and enter your P-Card information to complete the order.

-

Ordering Stationery Using a Purchase Order (PO)

You will need to create a Special Request requisition in order to be processed to a Purchase Order, which will then be used during the checkout portion in Step 2. When entering the Supplier ID, please use the following: 0000018027. Once a Purchase Order has been created from the requisition, continue to Step 2 to place your order.

Please note: the Office of Procurement does not order the stationery for your Department, but rather provides you with a Purchase Order number for you to place your order via the ordering portal.

After receiving the Purchase Order number, please proceed to the More Business Solutions ordering portal. At checkout, you will use the Purchase Order number in lieu of credit card number.

-

-

Printing Services

Generally, guidelines and procedures for other services apply to securing Printing Services. Please review the distinctions below.

-

Statewide Convenience Contracts

There are also resources made available by DOAS for obtaining printing Services through Statewide Convenience Contracts with:

- RR Donnelly (Offset Printing Services, SWC 99999-SPD-SPD0000096-0001)

- More Business Solutions (Rapid Copy & Digital Printing Services, SWC 99999-SPD-SPD0000108-0001)

- Georgia Correctional Industries (GCI) (SWC GCI-INTRGOVT)

When using these resources, purchasing limits do not apply and competitive bidding is not required.

To have the design/artwork pre-approved through the Office of Strategic Communications and Marketing, email requests to designapproval@kennesaw.edu prior to placing an order and/or making a purchasing.

Sales contact information for More Business Solutions is:

Eleanor Roath, Associate Vice President

5875 Peachtree Industrial Blvd., Suite 260, Peachtree Corners, GA 30092

T: 770.565.7772

E: eleanorroath@morebizz.net

Sales contact information for RR Donnelly is:Omar Kinnebrew, Assistant Regional Sales Manager

1117 Perimeter Center West, Ste. N201, Atlanta, GA 30338

T: 770.352.8472

C: 404.822.3188

F: 440.352.8404

E: omar.s.kinnebrew@rrd.com -

Talon Express - KSU Copy-Print Services

Talon Express is a mail center, print shop and retail outlet that offers a variety of services to students, faculty and staff including mail pick-up, full-service printing, copying, and shipping via USPS or UPS. It is located on the second level of the Carmichael Student Center, directly across from the Bursar’s Office.

To have the design/artwork pre-approved through the Office of Strategic Communications and Marketing, email requests to designapproval@kennesaw.edu prior to placing an order and/or making a purchasing.

Talon Express

http://talonexpress.kennesaw.edu/Contact: campusprintshop@kennesaw.edu

-

UGA Print Shop

KSU departments may also continue to use the UGA Print Shop to provide expanded printing/copying services. The UGA Print Shop handles bulk mailing and is a resource for banners and some signs.

Departments may contact the UGA Print Shop directly to discuss needs and obtain a quote. Contact information for UGA’s University Printing is located at http://www.printing.uga.edu/contactus.html.To have the design/artwork pre-approved through the Office of Strategic Communications and Marketing, email requests to designapproval@kennesaw.edu prior to placing an order and/or making a purchasing.

General Information, Quotes and Questions please contact Laura Cropp, Printing Estimator, at:

T: 706.542.3861

F: 706.542.7200

E: printing@uga.eduMore complex questions and/or guidance may require contacting:

Jeff Allen, UGA Print Shop Assistant Manager

T: 706.542-7195

E: hjallen@uga.eduFor quotes and additional support in utilizing the UGA Print Shop, you may contact:

-

-

Promotional Item Types

The University has several contracts for Promotional Items. These contractors were selected by an evaluation team from different university offices/colleges. A list of these items, the contracted suppliers, and their contact information is available below.

Merchandise or printed materials that incorporate University logos, service marks, or other University-related design elements must comply with KSU’s Visual Identity Program. To have the design/artwork pre-approved through the Office of Strategic Communications and Marketing, email requests to designapproval@kennesaw.edu prior to placing an order and/or making a purchasing.

Please note that suppliers listed on the Licensed Vendor page of KSU's Visual Identity Program are licensed ONLY to use the logo and do not constitute an existing University Contract.

The suppliers listed below are the preferred source(s) for promotional products as they have been awarded through a State-mandated competitive procurement process. In compliance with KSU's Visual Identity Program, the suppliers listed are licensed through Learfield Licensing Partners. If these suppliers do not meet your promotional items needs, you may select another supplier, registered with Learfield Licensing Partners, once justification documentation is submitted indicating the following:

If the requester prefers to use an alternate source, the College University Procurement Officer (CUPO) or Director of Contract Management may waive the use of the University Contract based on one of the following conditions below:- The Buyer Partner demonstrates that the University Contractor will not lower their price to match or be within 10 percent of the pricing of the non-contracted vendor.

- The cost savings from the non-contracted supplier is 10 percent or more.

- The product or service is needed quickly and cannot be delivered by the University contractor at the time needed.

-

Promotional ItemsThe KSU Office of Strategic Communications and Marketing has developed guidelines for various KSU designs, logos and typefaces on the KSU Visual Identity Program website.Merchandise or printed materials that incorporate University logos, service marks, or other University-related design elements must comply with KSU’s Visual Identity Program. You should also request a review from the Office of Strategic Communications and Marketing to alter existing approved brands or styles.

To obtain this approval, email your design ideas, concept and/or artwork to designapproval@kennesaw.edu prior to placing an order and/or making a purchase. After review, the Office of Strategic Communications and Marketing will reply to the requesting department, indicating that:- The design is approved for use;

- The design is approved with modifications; or

- The design is not approved.

-

Supplier Contact InformationHalo Branded Solutions, Inc.Contact: Dianne Helliwell PetersT: 770.321.4747Smiling Cross dba Smile PromotionsContact: Rula HananiaT: 812.219.9749F: 800.353.2608Club ColorsContact: Willis BreiT: 847.794.5496

-

-

Professional Services

-

Hiring a Caterer

Campus catering is managed in-house by Dining Services in the Office of Auxiliary Services and Programs. Any exceptions to using campus catering must be approved by Dining Services.

To begin planning your event, please complete the Catering Request form, email ksucatering@kennesaw.edu, or call 470-578-7715. -

Hiring a Consultant/Independent Contractor

Hiring Consultants/Independent Contractors follow similar requirements as outlined in “How do I Buy Services.” In addition, Human Resources approval is required to determine whether the individual is a current or past employee of the University System of Georgia, and if that’s the case, whether you can proceed with the hiring.

The Office of Legal Affairs should be contacted for assistance with contract development for the consultant/independent contractor that you need to hire only if modifications need to be made to the Independent Contractor Agreement template.

-

Employee vs. Independent Contractor

Federal and state tax and labor laws require Kennesaw State University (KSU) to ensure that individuals who provide services are properly classified as an employee or an independent contractor. Proper classification of an individual will determine Kennesaw State University’s tax withholding and reporting obligations.

To assist in proper classification, please use the Independent Contractor vs. Employee Checklist.

Individuals who perform services for KSU are presumed to be employees unless the relationship, supported by documentation, satisfies the Internal Revenue Service (IRS) and state law standards for an independent contractor status. Individuals who receive a Form W-2 from KSU should be paid as an employee for all services provided and typically should not also receive a Form 1099 from KSU.

KSU’s Office of Procurement works collaboratively with the Office of Compliance, Division of Legal Affairs, and Department of Human Resources to determine the classification categories of payments to individuals.

Please see the University's Consulting Services Policy for more information.

-

Classification of an Employee

An employee is a person hired through Kennesaw State University’s Department of Human Resources and paid via Payroll. KSU controls and directs this person's activities, both in terms of what must be done and how it must be done. An employee may be classified as a permanent full-time employee, part-time employee or as a temporary employee. Generally, employees will always be paid through the payroll system even if the duties they perform are unrelated to their primary role.

Some Examples of Characteristics of an Employee

- Performs duties dictated or controlled by others

- Is given training for work to be done

- Teaches a course from which students may receive academic credit

- Performs trade type duties, e.g., clerical, janitorial, grounds keeping services, lab technicians.

Please note that when KSU engages a temporary agency to provide trade type services, the agency, and not the individual, will be considered an independent contractor.

-

Classification of an Independent Contractor

An independent contractor (also referred to as contractor, consultant, freelancer, etc.) may be an individual or sole proprietor that renders services to the general public. An independent contractor is responsible for the means and methods for completing a task based on specifications in a contract with KSU. An independent contractor generally has multiple clients, maintains a separate workplace, is not supervised or controlled by a KSU employee, and does not receive KSU benefits.

Examples of characteristics of an independent contractor:

- Operates under a business name

- May have his/her own employees

- Maintains a separate business bank account

- Advertises his/her business services

- Invoices for work completed

- Has own tools and sets own hours

- Keeps business records

-

Classification of Non-US Tax Resident Individuals

Individuals who are not U.S. citizens or permanent legal residents (green card holders) may be subject to a variety of restrictions on employment or independent contractor services. All non-employee service providers who perform a service on U.S. soil must initiate a GLACIER tax compliance record, including a review of immigration documentation, prior to initiation of a requisition, an invitation, a service agreement, or verbal commitment to make payment. Please contact hr@kennesaw.edu or submit a ServiceNow request via service.kennesaw.edu/ofs for additional guidance.

-

Kennesaw State University Policies and Procedures

-

What is the Consequence of Misclassification?

Misclassification of an individual as an independent contractor may have a number of costly legal and financial consequences for the University. Consequently, it is essential that proper characterization of an individual be determined before any agreements, contracts (oral or written) or payments are made. The fundamental difference between an employee and independent contractor from a tax point of view is that an employer withholds employment taxes, and pays FICA taxes on its employees.

If an independent contractor is discovered to meet the legal definition of an employee, the University may be liable for:

- Wages that should have been paid to them under the Fair Labor Standards Act, including overtime and minimum wage

- Back taxes and penalties for federal and state income taxes, Social Security, Medicare and unemployment

- Any misclassified injured employee's workers' compensation benefits

- Employee benefits, including holiday pay, health insurance, retirement, etc.

-

-

-

Hiring a Doctor, Lawyer or Other Professional

Licensed professions are exempt from the State’s competitive bidding requirements. Licensed professions include architects; counselors/social workers; surveyors; nurses; real estate appraisers; engineers; accountants (CPA’s); attorneys.

E-verify Affidavits are not required for service contracts entered into with licensed professional contractors/sub-contractors. However, contract requirements as outlined in “How do I Buy Services” do apply. Contact the Office of Procurement for additional guidance for procuring services in this area. -

Hiring a Lecturer

Speakers and lecturers are exempt from State purchasing guidelines for competitive bidding (Exempt NIGP Code 91838). HR approval is required and E-verify compliance (Affidavit or Driver’s License) applies if service provided is equal to or greater than $2,500.00.

The Lecturer Agreement form and additional travel expense rider, if needed, can be found on the Contract Management System by clicking on "View My Templates" on the bottom left side of the homepage.

A list of FAQs regarding travel for Lecturers and Performers can be found on Travel's website.

-

Hiring a Skilled Practitioner

Licensed professions are exempt from the State’s competitive bidding requirements. Licensed professions include, but are not limited to:

- Accountants & CPA’s (Exempt Code 946);

- Architects (Exempt Codes 906 & 907);

- Attorneys (Exempt Code 918);

- Counselors (Exempt Code 952);

- Engineers (Exempt Code 925);

- Nurses (Exempt Code 948);

- Real estate appraisers (Exempt Code 946);

- Surveyors (Exempt Code 925)

E-verify Affidavits are not required for service contracts entered into with licensed professional contractors/sub-contractors. However, contract requirements as outlined in “How do I Buy Services” do apply.

-

Hiring a Temp

Departments should contact Human Resources before attempting to hire a temporary employee. HR approval is required to determine whether the individual is a current or past employee of the University System of Georgia; and if that is the case, whether you can proceed with the hiring. After consultation with HR, you may post a requisition for a temporary position through OneUSG or use one of the statewide contracts for non-licensed professions or support staff.

If you would like to hire a temporary person directly, meaning they will be on payroll, please contact Human Resources.

What if my purchase order is not enough to cover the original request? Submit an ePro Special Request to add additional funds to the existing purchase order.

Can a temporary employee supervise permanent full-time staff? Please contact Human Resources.

If KSU is closed for a paid holiday, do I still pay my temporary employee? No, temporary personnel only get paid for the hours they actually work. You will need to verify and approve the temporary employee's time.

What if the temporary employee is not working out for our department and we no longer want that person? Call the temporary agency and let them know the situation. You can either have that temporary employee replaced with another temporary employee from that agency or try one of the other temporary agencies from the mandatory statewide contract.

What if we really like the temporary employee and want to hire them as permanent staff? Each temporary agency has schedules and sliding scale payment ranges for placement fees. First, ensure your department has the budget for the position. Second, check with Human Resources to see if the Critical Hire status is still in effect and what needs to be done for the next steps. Third, contact the temporary agency for any potential buyout requirements, and if required, obtain a quote, in order to permanently hire the temporary employee.

-

-

Technology Purchases

-

GSA Schedule 70 - General Purpose Commercial Information Technology Equipment, Software, and Services

These contracts may be used by the University under the Cooperative Purchasing guidelines authorized by the Department of Administrative Services – State Purchasing Division. One of the requirements for use of these contracts is the posting of a public notice on the Georgia Procurement Registry for five to fifteen days depending on the dollar amount - see Georgia Procurement Manual (GPM) Section 1.3.4.4. Consortia or Cooperative Purchasing. Contracts with the COOP PURC icon indicate that authorized state and local government entities may procure from that contract. You may view a list of the contract types at the following link:

https://www.gsaelibrary.gsa.gov/ElibMain/scheduleSummary.do?scheduleNumber=70&id=71

-

Purchasing a Computer

Please visit the Technology Purchases website, click on the "Computers, Servers and Peripherals" link, complete the form and choose "Submit" to obtain UITS approval for the purchase.

Once you receive UITS’s approval, create an ePro Special Request with the quote attached. Once the request is fully approved through the ePro workflow, a Buyer in Procurement will issue a purchase order and notify you when the purchase order is sent to the supplier.

-

Purchasing Cell Phone Service

KSU cellular phones and services can be requested through UITS. The completed form requires signatures from the employee, the department head, and the Chair/AVP prior to submission to the office of the CIO for final approval. Currently there are accounts and service with AT&T, Verizon and other suppliers. A complete list of cell phone suppliers is available from the Georgia Technology Authority (GTA) website.

-

Purchasing a Printer

To purchase desktop printers and desktop multifunction devices, please visit the Technology Purchases website, click on the “Computers, Servers and Peripherals” link, complete the form and choose “Submit” to obtain UITS approval for the purchase.

Once the department receives UITS’s approval, and sometimes a quote for the requested equipment is provided by UITS if needed, an ePro Special Request is submitted by the Requester for the Buyer in the Office of Procurement to create a purchase order. You will then be notified that the purchase order was sent to the supplier/seller.

-

Purchasing a Projector

To purchase cameras, projectors, microphones, camcorders rental equipment for events or specialized recordings, and out-sourcing of production for videos and interactive media, go to the Technology Purchases website and click on the “Audio/Visual Rentals, Purchases, and Related Services” link. Fill out the form and choose “Submit” to obtain UITS approval for the purchase.

Once you receive UITS’s approval and a quote provided by UITS (if needed), create an ePro Special Request. After the requisition goes through the approval workflow, a Buyer in Procurement will issue a purchase order and notify you that the order is complete.

-

Purchasing Software, Web Hosting or Web Applications

Please visit the Technology Purchases website, click on the “Software and Related Services Purchases” link, complete the form and choose “Submit” to obtain UITS approval for the purchase. Procurement processing time will depend on the dollar value. If the item or service is less than $25,000 but more than $10,000, three quotes should be attached to the ePro Special Request.

- If the cost is greater than $25,000 but less than $250,000, an eQuote or Request for Proposal may be required and could take up to sixteen weeks. Technology purchases over $250,000 require special additional approval and require more time for approval. Please allow for at least 4 weeks for the additional approval.

Please note that if a contract is required by the supplier (seller) in order to purchase the software, web hosting, or web application, then the Contracts Office must review and approve the proposed contract. In order for the Contracts Office to review the contract, please complete the Contract Submission Form.

If the desired product/service is being procured from a University, Board of Regents, or Statewide contract, then additional review from the Contracts Office is not needed, unless customizations and/or modifications to the product/service is required for successful use by the University.

If use of the software or application requires the Seller to provides service such as maintenance, product development, offsite hosting, etc.), and the cost is $2,500 or more, then E-verify compliance is required.

-

-

Travel & Charter Services

-

Booking a Flight

KSU Travel policy requires employees to use the Concur online tools for travel requests, travel cash advance requests, travel bookings (airline, hotels, and car rentals), and travel expense reports. To begin using Concur, please complete the Concur User Profile Action Form, which is located on the Travel website. The form should be completed and emailed to the KSU Travel Administrator at service.kennesaw.edu/ofs.

-

Buying a Vehicle

In order to purchase a motor vehicle, you must first consult with the KSU Fleet Manager in the KSU Office of Facilities Planning and Design, then draft a justification letter for the signature of the Chief Business Office for prior written approval of DOAS’s Fleet Management Division is required. Approval is required even if an existing statewide contract is being utilized to acquire the vehicle. Contact Fleet Management Division online or email FMS@doas.ga.gov.

-

Renting a Vehicle

Enterprise Leasing Company of GA LLC and The Hertz Corporation are the suppliers for in-state car rentals under MANDATORY Statewide Contract number’s 99999-SPD-ES40199376IS-02 and 99999-SPD-ES40199376IS-01, respectively.

The Hertz Corporation is the MANDATORY supplier for all airport rentals at Georgia, national and international airports under Statewide Contract number 99999-SPD-ES40199376CR-01.

Kennesaw State University and the State implemented online booking (TTE), also known as Concur, for booking airfare, hotel and rental car reservations. Concur may be accessed via the following link: https://www.concursolutions.com/. To obtain initial access to Concur, please contact the Travel Team at service.kennesaw.edu/ofs or contact the Travel Hotline at (470) 578-4394.

Approved car rental sizes are Compact, Intermediate or Full Size. Other vehicle sizes require a business-related justification. Vans may be rented when there are more than four (4) travelers. -

Chartering a Bus

AutoMax Rent-A-Car is under contract with the State for charter bus service (SWC #99999-SPD-ES40199376BS-01). Reservations for 15 Passenger Buses and other bus types can be made on-line by:

- Logging on to automaxrental.com.

- Fill out the request for quote.

- You will need your driver’s license and state employee identification card to rent a vehicle.

- Reservations can be made by calling Bus Max at one of the three locations: Cartersville – (770) 607-7000; Norcross – (770) Bus-Rent; Rome – (706) 291-0600

KSU Departments and Student Organizations may also charter bus service (up to 35 passengers within a 50-mile radius) through the Department of Parking and Transportation with the Big Owl Bus (B.O.B.) for special events, field trips, conferences, etc.

Please visit the KSU Charter Services Policy website for more information.

-

-

Words and Terms to Know When Purchasing a Good or Service

-

Convenience Statewide Contracts

State entities may, but are not required to, use a convenience statewide contract. They offer several benefits in terms of saving time and ensuring compliance with procurement rules, as pricing and contract terms have already been finalized, and are not limited by dollar amount.

-

Mandatory Statewide Contracts

State entities are required to use mandatory statewide contracts, unless a written waiver is granted by the State Purchasing Division (SPD). Similar to Convenience Statewide Contracts, Mandatory Statewide Contracts are not limited by dollar amount.

-

Exempt Purchases

Exempt Purchases are either exempt from the State Purchasing Act or represent goods for which SPD has waived the competitive bidding requirements. The fact that a purchase may be exempt is not a representation that the purchase may not need to be competitively bid.

-

Marketplace Catalog

This is a list of items that have been competitively bid by the State and are contractually sourced. These items appear on the GeorgiaFIRST Marketplace in ePro and are not limited by dollar amount.

-

Punch-Out Supplier

These are Suppliers on the GeorgiaFIRST Marketplace that allow the Requester to search and select products from that supplier’s web catalog (i.e., Dell’s Government Catalog) by navigating directly to the Punch-Out Supplier's website. The Requester then returns the items to the GeorgiaFIRST Marketplace shopping cart. Punch-Out catalogs still maintain items and pricing specific to the University System of Georgia.

-

-

-

eVerify

-

E-Verify Contractor Requirements

Georgia law, O.C.G.A. § 13-10-91, requires all businesses that contract with a public employer for labor or services by bid or by contract in which the labor or services exceed $2,499.99 to sign an affidavit attesting that they are registered for and use E-Verify unless

- the contractor has no employees (in which case they must present an approved state issued identification card/drivers’ license from an approved state as provided on the Attorney General’s website) or,

- the contract is with an individual licensed under Title 26, Title 43, or the State Bar of Georgia who is in good standing and that individual is performing that service.

Anyone your business subcontracts with for labor and services, as well as the subcontractors of your subcontractors, in furtherance of that contract is also subject to this requirement.

-

E-Verify Private Employer Requirements

Georgia law, O.C.G.A. § 36-60-6, requires all businesses, with more than 10 employees that are seeking an occupation tax certificate/business license or other document required to operate a business with a county or city to sign an affidavit attesting that they are registered for and use E-Verify. Businesses with 10 or fewer employees are required to sign an affidavit attesting that they are exempt from this requirement.

Once a business has provided this affidavit to the county, all subsequent renewals can be provided with the submission of the E-Verify number, as long as it is the same number as provided on the affidavit, or assertion that your business is exempt. The county will provide the format in which renewal information is collected.

-

What Is E-Verify?

E-Verify is a federal Web-based system that electronically verifies the employment eligibility of newly hired employees. It works by allowing participating employers to electronically compare employee information taken from the I-9 Form (the paper-based employee eligibility verification form used for all new hires) against records in the Social Security Administration's database and the records in the Department of Homeland Security immigration databases.

-

Where Do I Find My E-Verify Number?

The Human Resources Department for your business should have that information, if you have registered. The E-Verify number, which consists of four to six numerical characters, is located directly below the E-Verify logo on the first page of the memorandum of understanding (MOU) entered into between your business and the Department of Homeland Security (DHS) to use E-Verify.

-

What if I cannot locate or do not have access to my MOU?

If the HR director/program administrator for E-Verify from your business has taken the E-Verify tutorial, you may obtain your company ID number by:

- Logging in to E-Verify with your assigned user ID and password;

- From 'My Company,' select 'Edit Company Profile;'

- The Company Information page will display the company ID number.

If your HR director/ program administrator has not completed the tutorial, you must contact E-Verify Customer Support at 888-464-4218 or at E-Verify@dhs.gov for assistance.

-

Is the Federal Tax Identification Number/Employer Identification Number (EIN) the same as the E-Verify Number?

No. While you will be required to provide the Federal Tax Identification Number/EIN for your business to DHS in order to register for E-Verify, a separate number, which consists of four to six numerical characters, will be provided as the E- Verify number for your business by DHS, which will be located on the MOU.

-

How Do I Register for E-Verify?

To register for E-Verify, please visit the DHS website. If you need assistance in completing the registration process or need additional information relating to E-Verify, call their customer service number at 1-888-464-4218, email them at E-Verify@dhs.gov or visit their website.

-

What is the definition of a service?

Clarification from DOAS’s State Purchasing Division (SPD) and the AG’s Office has been sought. However, in general, the advice provided by DOAS SPD is to “err on the side of caution and obtain the affidavit.” For the purposes of determining whether or not something is a good or a service, use this rule as a simple distinction: a good is tangible and a service is intangible. If you have additional questions, please do not hesitate to contact service.kennesaw.edu/ofs or call (470)578-6214.

-

Do I need to get the eVerify affidavit, or will Procurement and Contracting obtain it?

The Office of Procurement and Contracting will obtain all required affidavits from vendors that are issued PO's in PeopleSoft. However, to expedite the processing of a requisition, end-users may obtain the affidavits on their own and attach it to their requisition.

-

Do I need to get an eVerify affidavit for P-Card purchases?

Yes, eVerify rules apply to ALL purchases that meet the criteria listed in question number one above.

-

If my purchase requirement for services is an exempt commodity (meaning that it is exempt from bidding requirements), is my purchase exempt from eVerify requirements?

No. eVerify requirements are different from bidding requirements. eVerify affidavits are required for ALL purchases that meet the criteria listed above, even if they are considered an exempt commodity.

-

Where can I find the eVerify instructions and affidavit form?

The Security and Immigration Compliance Affidavit form and related instructions can be found towards the top of this page under "Documents and Links Referenced in This Section".

-

-

Contracts

-

How do I know if KSU has a contract for a certain Supplier or a certain type of goods?You may reach out to Procurement either by ServiceNow, service.kennesaw.edu/ofs, or by phone, 470.578.6214

-

How long does a contract take to be awarded?The length of time for a contract to be awarded to a supplier varies depending on the complexity of the solicitation. We would ask that you allow at least eight weeks for RFQs and sixteen weeks for RFPs. Again, the more complex the RFQ or RFP is, the longer it can take.

-

I have an emergency on campus and the cost is expected to be over $25,000 ($50,000 for Public Works). Is there a way to expedite the process?Per DOAS rules, emergencies do not require the use of a competitive solicitation, but they do require notification to Procurement within 24 hours so that we may coordinate with DOAS to allow work to begin immediately. Please reach out to Procurement as soon as possible to avoid any violations of State rules.

-

List of Statewide Convenience and Mandatory Contracts

A complete list of State contracts can be found on the Team Georgia Marketplace. Please note that the User Name and Password are both “tgmguest" (all lowercase and without quotes), as shown below:

-

What is an E-Verify Affidavit and why is it needed?

Effective July 1, 2013, an E-Verify affidavit is required:

When a public employer makes a purchase that includes services or labor, and the total amount of a purchase exceeds $2,499.99.

-

What is the threshold for purchases made during the fiscal year that would require competitive bidding?

A competitive solicitation is required for any purchases $25,000 or more that are non-exempt and are not already on Statewide Contract. This does not include Public Works Contracts, which is anything $50,000 or more.

-

-

eProcurement (ePro)

Please view our job aid page for more instructions on creating, approving, and maintaining requisitions (errors, issues, and more).

- Accounting Date Error - Please contact your Buyer Partner or submit a ServiceNow request via service.kennesaw.edu/ofs to update the accounting date of the requisition you are trying to edit.

- Budget/Project Manager Setup Changes - Contact budget@kennesaw.edu for changes to budget owners and project managers.

- Business Manager Setup Changes - Contact pssecurity@kennesaw.edu for changes to business managers.

- Can't Log In - If you are an approver and can no longer log in, you likely did not resubmit for PeopleSoft Access. This is done annually, please fill out the access form to gain access again.

- Clearing Browser Cache - Browser errors can often be cleared by clearing out the cache.

- Do I Need E-Verify? - Per the State Accounting Office (SAO) Statewide Purchase Orders Policy, all purchases $2,500 or more must be procured using a Purchase Order (PO). For purchases involving services $2,500 or more, an E-Verify Affidavit is required. For more information regarding E-Verify, please see the E-Verify FAQ page.

- Requisition Status - Instructions on how to look up the status of your requisition/purchase order.

-

Invoice Payment

For all invoices associated with a Purchase Order (PO), please submit the invoice via ServiceNow to service.kennesaw.edu/ofs and indicate the PO number that the invoice is being paid against. You do not need to submit a Payment Request to pay for an invoice that has a PO associated with it, as you will be encumbering funds twice.

For any invoices that do not have a PO associated with them, please submit a Payment Request if the purchase is not allowable on P-Card. A PO cannot be issued after the purchase has been made as this is an after-the-fact purchase.

-

Payment Request

For Payment Request inquiries and questions, please visit the Accounts Payable section of the Fiscal Services site.